REVERSE BURDEN OF PROOF

BY S. K. VERMA, ADVOCATE – 02.04.2026-13:28

REVERSE BURDEN OF PROOF UNDER SECTION 123 OF THE CUSTOMS ACT, 1962

1. Introduction

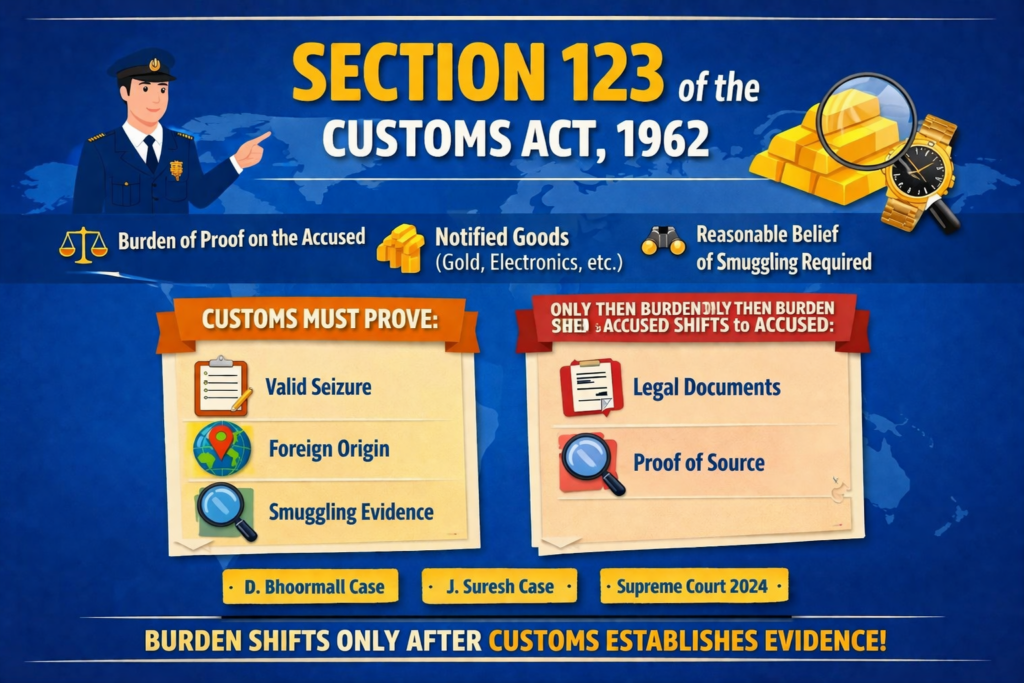

Section 123 is a reverse burden of proof provision in customs law. It shifts the burden of proof from the prosecution to the accused in cases involving notified goods (like gold) suspected to be smuggled.

However, modern judicial interpretation—especially by the Supreme Court—has ensured that this provision is not applied mechanically.

REPRODUCTION OF SECTION 123 OF THE CUSTOMS ACT, 1962 IS AS BELOW:-

- 123. Burden of proof in certain cases.[(1) Where any goods to which this section applies are seized under this Act in the reasonable belief that they are smuggled goods, the burden of proving that they are not smuggled goods shall be-(a)in a case where such seizure is made from the possession of any person,-(i)on the person from whose possession the goods were seized; and(ii)if any person, other than the person from whose possession the goods were seized, claims to be the owner thereof, also on such other person;(b)in any other case, on the person, if any, who claims to be the owner of the goods so seized.](2)This section shall apply to gold, [and manufactures thereof,] [ Substituted by Act 40 of 1989, Section 2, for ” diamonds, manufacturer of gold or diamonds” .] watches, and any other class of goods which the Central Government may by notification in the Official Gazette specify.

2. Latest Supreme Court Position (2023–2025 Developments)

(A) Settlement Commission & Section 123 – Split Verdict

Yamal Manojbhai v. Union of India

Issue: Whether a person dealing with Section 123 goods can approach the Settlement Commission under Section 127B.

Bench: Justice Krishna Murari & Justice Sanjay Karol

Result: Split verdict → matter referred to larger bench

Key Observations

Does Section 123 create a reverse burden of proof (accused must prove innocence)?

![]() Latest Position:

Latest Position:

Law is not finally settled—issue pending before a larger bench.

B. Supreme Court Principle on “Reasonable Belief” (Continuing Authority)

Collector of Customs v. D. Bhoormall

This remains the leading precedent repeatedly relied upon in recent cases (including 2025 decisions):

Customs need not prove smuggling with mathematical certainty.

Standard is:

“What a prudent man would believe” �

![]() Principle reaffirmed in 2025 litigation:

Principle reaffirmed in 2025 litigation:

“Reasonable belief” = probability-based, not absolute proof

(C) Supreme Court Requirement: Proof of Foreign Origin

Ganesh Das v. Collector of Central Excise

Commissioner of Customs v. Abdul Gani

These judgments are consistently followed in latest tribunal rulings (2024–2025):

Before shifting burden under Section 123:

Customs must show foreign origin or smuggling indicators

Mere suspicion is insufficient.

![]() Modern Position (Reaffirmed): Section 123 does not eliminate initial burden.

Modern Position (Reaffirmed): Section 123 does not eliminate initial burden.

3. Important Tribunal & Recent Developments (2024–2025)

(A) No Evidence → No Section 123

2024 CESTAT:

Section 123 not applicable without proof of foreign origin.

Taxscan

(B) Domestic Seizure Cases (2025)

If gold is seized within India (not at border):

Customs must prove smuggling first

Burden does not automatically shift. �

(A) J. Suresh v. Commissioner of Customs

Held:

“Reasonable belief” must be based on objective material

Section 123 fails if belief is arbitrary

![]() Reinforces Supreme Court standard of “prudent belief”

Reinforces Supreme Court standard of “prudent belief”

(B) Daleep Kumar Verma v. Commissioner of Customs

Held:

Burden does not shift unless:

Foreign origin OR

Smuggling circumstances shown

![]() Aligns with SC rulings in:

Aligns with SC rulings in:

Ganesh Das

Abdul Gani

5. Consolidated Legal Position (After Latest SC Developments)

Step 1: Customs Must Establish

Seizure under Act

Goods are notified

Reasonable belief (prudent man test)

Some evidence of smuggling/foreign origin

Step 2: Only Then Burden Shifts

Accused must prove:

Lawful import

Legitimate possession

6. Key Legal Principles (Modern Doctrine)

(i) Reverse Burden is Conditional

Not automatic

Triggered only after threshold proof

(ii) Reasonable Belief = Prudent Man Standard

Not suspicion

Not guesswork

(iii) Foreign Origin is Crucial

Especially in inland seizures

(iv) Section 123 is Strictly Construed

Being an exception to criminal law principles

7. Critical Analysis (With Latest SC Insight)

Judicial Trend

Courts (including Supreme Court) are:

Narrowing misuse of Section 123

Ensuring procedural fairness

Protecting presumption of innocence

Pending Constitutional Issue

Settlement Commission jurisdiction (Yamal Manojbhai case)

![]() Could significantly impact future interpretation

Could significantly impact future interpretation

8. Conclusion

The latest Supreme Court position shows that:

Section 123 is not a blanket presumption tool

It is a carefully controlled evidentiary exception

With cases like:

Yamal Manojbhai v. Union of India

Collector of Customs v. D. Bhoormall

Ganesh Das v. Collector of Central Excise

the law today is clear:

Reverse burden arises only after Customs proves a credible foundation.